Outsourcing for UK practices can be a huge money saver – till it’s not. The difference between meeting your cost-saving goals and falling short often comes down to the outsourcing model chosen. While a cheaper model might seem tempting at first, in the end it really boils down to the value i.e. the value you receive for the cost.

This is perhaps why it’s so important to take the time to understand the outsourcing models and their providers. This critical decision often shapes your long-term partnership which includes how risks are shared, what the best possible outcomes look like, and the values that drive both teams. While this matters in outsourcing, in the world of finance, the impact of this partnership is further amplified.

Outsourcing models themselves suit different kinds of practices and workloads, and getting the match wrong is an expensive fix especially end of the project. This blog looks at how the models for accounting outsourcing UK actually work in practice, how they apply to each type of practice, and how to tell which one is right based on its own situation.

What are the popular outsourcing pricing models for UK firms

Most outsourcing arrangements in the UK accounting sector involve two outsourcing pricing models UK firms, with a few hybrids frameworks that also exist. Understanding the underlying logic of each is the key to getting started. The logic behind the individual models is what determines how they behave once the work starts flowing.

Fixed price: paying for an outcome

Fixed price outsourcing UK accountants ties the fee to a defined scope of work rather than the effort involved in delivering it. The practice agrees what gets done, the provider quotes a set figure, and that figure holds regardless of how long any individual job takes.

A practice might agree to pay a monthly fee for a set number of bookkeeping outsourcing clients, or a fixed cost per set of year-end accounts, or a flat monthly retainer covering an agreed bundle of work. The defining feature is that the price is known in advance and does not move with the hours expended.

Per-task: paying for what gets done

Per task outsourcing accounting charges for each unit of work as it is completed. A fee per VAT return, a rate per set of accounts, a price per personal tax return, a charge per payroll run. The practice pays for what it sends, and nothing for what it does not.

This is the model that scales with activity rather than commitment. In a quiet month, the cost falls. In a busy month, it rises. The fee tracks the actual volume of work passing through the arrangement.

Table: Fixed Price vs Per Tax vs Managed FTE outsourcing models

| Criteria | Fixed Price | Per-Task | Managed FTE |

|---|---|---|---|

| Cost Predictability | High | Low | High |

| Flexibility | Low | High | Medium |

| Best for Seasonal Work | No | Yes | No |

| Best for Stable Workloads | Yes | No | Yes |

| Scalability | Medium | High | High |

| Margin Visibility | High | Medium | High |

| Long-Term Cost Efficiency | High | Medium | Very High |

The third option: managed FTE

The fixed-versus-per-task argument leaves out a model that a large share of UK practices actually employ, and any real apple-to-apples comparison has to include it. Managed FTE, i.e. a dedicated full-time equivalent, sits somewhere between the two. The practice pays a fixed monthly fee for a named offshore resource, or a team of them, assigned to its work under UK supervisory oversight.

Indicative 2026 market rates put an entry-level FTE handling bookkeeping, bank reconciliation, and basic VAT at roughly £1,400 to £1,600 a month. A qualified, accountancy-grade FTE covering management accounts, year-end preparation, and tax computations run closer to £1,800 to £2,400, with senior or managerial resources higher again. Against a UK hire at £3,500 to £4,500 a month fully loaded, the gap is the whole point.

Managed FTE pricing table

| Resource Type | Typical Monthly Cost |

| Junior Bookkeeping FTE | £1,400-£1,600 |

| Mid-Level Accounting FTE | £1,800-£2,400 |

| Senior Accountant FTE | £2,500-£3,500 |

| Team Lead / Manager | £3,500-£5,000+ |

Managed FTE looks like fixed price outsourcing UK accountants in that the monthly cost is known. It differs in what the practice is buying. Fixed price buys a defined output. Managed FTE buys reserved capacity, a set number of hours, rather than a guaranteed set of completed jobs. That distinction matters more than it first appears, and it’s one of the most common sources of confusion when practices compare quotes.

Billing unit versus engagement model

A point worth making before going further, because it clears up a lot of muddled comparisons: the billing unit and the engagement model are not the same thing, even though providers often blur them.

The billing unit is how the fee is calculated, per job, per hour, per FTE, per month. The engagement model is how the practice and provider actually work together, whether the resource is dedicated or shared, how review is structured, and who owns the client relationship. A managed FTE is a billing unit. A dedicated team constitutes a type of engagement model. They tend to travel together, but they are separate decisions and treating them as identical is how practices end up paying for reserved capacity while assuming they’ve bought guaranteed outcomes.

| Pricing Method | Typical Usage |

|---|---|

| Per VAT Return | Compliance work |

| Per Tax Return | Self-assessment services |

| Per Payroll Run | Payroll processing |

| Fixed Monthly Fee | Bookkeeping & recurring services |

| Dedicated FTE | High-volume outsourcing |

| Hourly Billing | Ad-hoc projects |

Where does fixed price outsourcing work for UK accountants

Fixed price tends to suit practices with predictable, steady workloads and a preference for budget certainty over flexibility. There is a particular kind of firm for which it is close to ideal and recognising whether a practice fits that profile is the first step.

Predictable volume is the prerequisite

The fixed price outsourcing UK accountants model rewards predictability. A practice that processes roughly the same volume of work month after month, with a stable client base and few dramatic seasonal swings in a given service line, gets the most from it. The provider can price the arrangement accurately because the workload is knowable, and the practice gets a cost it can build into its own budgeting without surprises.

Where the volume is genuinely stable, fixed price also tends to produce a better unit cost than per-task would. The provider is taking on less uncertainty, and that reduced risk is usually reflected in a keener price. Predictability, in other words, is something the practice can monetise.

Budgeting and margin protection

| Item | Fixed Price Model | Per-Task Model |

|---|---|---|

| Client Fee Charged | £250 | £250 |

| Average Outsourcing Cost | £100 | £80-£140 |

| Gross Margin | £150 | £110-£170 |

| Margin Predictability | High | Low |

For a practice that bills its clients on a fixed fee, which is a major share of the profession, a fixed price outsourcing arrangement aligns neatly with how the revenue side works. The cost base and the revenue base move on the same logic. The practice knows its outsourcing cost per client, knows what it charges that client, and knows its margin with confidence.

That alignment is harder to achieve under a per task outsourcing accounting model, where the cost can move in a month when the revenue does not. For firms that have built their commercial model around predictable client fees, fixed price outsourcing protects the margin in a way per-task can struggle to match.

The scope discipline it demands

Fixed price only works when the scope is genuinely fixed. The model’s weakness is scope creep. If the agreed bundle quietly expands, an extra report here, a more complex client there, a few additional tasks that were never priced in, the economics tilt against whichever party absorbs the unscoped work.

Well-run fixed price arrangements therefore depend on a clearly documented scope and a disciplined process for handling anything that falls outside it. The practices that struggle with fixed price are usually the ones that treated the scope document as a formality. The ones that thrive treat it as the thing that keeps the arrangement fair to both sides.

When does per-task outsourcing accounting make sense

Per task outsourcing accounting suits practices with variable, unpredictable, or seasonal workloads, and those that want to pay only for what they use without committing to a fixed bundle. It is the more flexible model, and flexibility has real value in the right circumstances.

Seasonal and variable demand

The clearest case for per task outsourcing accounting is the practice whose workload spikes and troughs across the year. Personal tax work concentrated around January. Year-end accounts clustered around particular financial year-ends. P11D work bunched after the tax year closes. For a firm whose outsourcing need swells and recedes with the calendar, per-task means paying for the swell without carrying the cost through the trough.

A fixed monthly retainer sized for the busy period would be poor value in the quiet months. A retainer sized for the quiet period would not cover the busy ones. Per-task sidesteps that mismatch entirely by tracking the actual work.

| Service Line | Seasonality |

|---|---|

| Bookkeeping | Low |

| Payroll | Low |

| VAT Returns | Medium |

| Corporation Tax | Medium |

| Year-End Accounts | High |

| Personal Tax Returns | Very High |

| P11D Reporting | Very High |

Testing a provider before committing

Per-task also serves as a lower-commitment way to begin a relationship with a new outsourcing partner. A practice that is not yet ready to commit to a fixed monthly arrangement can send discrete pieces of work, assess the quality and turnaround, and build confidence before deepening the relationship.

This matters because the cost of a bad outsourcing relationship is not just the fee. It is the disruption, the rework, and the client-facing consequences when something goes wrong. Per-task lets a firm test the water at a manageable risk before wading in.

Per-task also serves as a lower-commitment way to begin a relationship with a new outsourcing partner. A practice that is not yet ready to commit to a fixed monthly arrangement can send discrete pieces of work, assess the quality and turnaround, and build confidence before deepening the relationship.

This matters because the cost of a bad outsourcing relationship is not just the fee. It is the disruption, the rework, and the client-facing consequences when something goes wrong. Per-task lets a firm test the water at a manageable risk before wading in.

The variability trade-off

The flexibility of per-task comes with a cost, and that cost is predictability. A practice on a per-task model cannot forecast its outsourcing spend as precisely as one on a fixed arrangement. In a busier-than-expected period, the bill is higher than budgeted.

For some firms that is an acceptable trade. The cost rises in the months when the revenue is also rising, so the practice can usually absorb it. But a firm that needs tight cost certainty, or that struggles to pass variable costs through to clients, may find the unpredictability uncomfortable. The model that flexes with demand also flexes with the budget.

What is the right outsourcing model for my practice

The honest answer to which model works best is that it depends on the practice, and specifically on a small number of characteristics that are worth assessing directly rather than assuming.

Questions a firm should ask itself

- Volume stability. A practice with steady, predictable throughput in a service line is a natural fit for fixed price in that line. One with sharp seasonal peaks is better served by per-task, at least for the seasonal work.

- How the practice bills its own clients. Fixed-fee client billing pairs naturally with fixed price outsourcing. Time-based or variable client billing sits more comfortably alongside per-task.

- Appetite for cost certainty versus flexibility. Some firms value a predictable cost base above all else. Others would rather pay only for what they use and accept the variability that comes with it. Neither preference is wrong, but they point to different models.

- Stage of the partnership. A new, untested outsourcing relationship often makes sense to begin on a per-task basis and migrate to fixed price once trust and predictable volume are established.

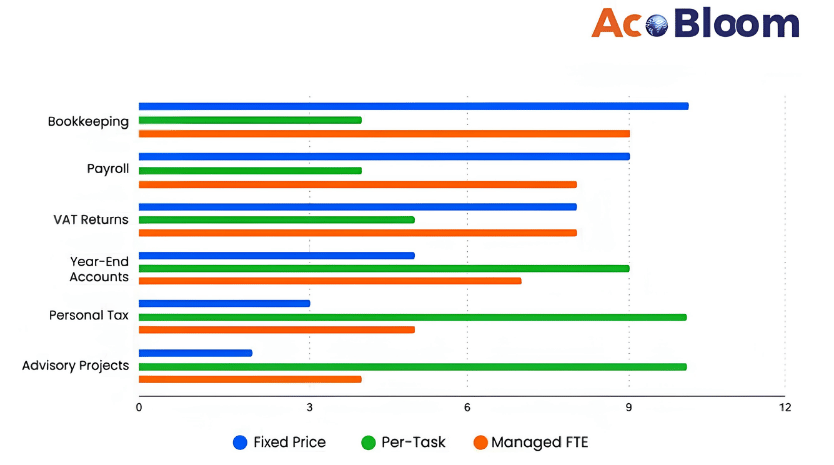

Suitability of Outsourcing Models by Service Type

The hybrid approach most mature arrangements settle into

In practice, many established outsourcing relationships end up combining both models rather than choosing one outright. A practice might put its steady, predictable work, routine monthly bookkeeping, for instance, on a fixed price basis, while handling its seasonal personal tax surge on a per-task basis.

This is often the most rational structure. It applies fixed price where predictability makes it efficient, and per-task where variability makes flexibility valuable. Firms that get the most from outsourcing are frequently the ones that stopped treating the choice as binary and instead matched the pricing model to the nature of each stream of work.

Why the binary framing misleads

Framing the decision as fixed price versus per-task, as though a practice must pick one and apply it to everything, is the error that leads to poor fits. A firm’s work is not homogeneous. Some of them are predictable and some seasonal. Some align with fixed client fees, and some do not.

A provider worth working with should be willing to structure the arrangement around the requirements of practice client tasks, rather than pushing a single pricing model because it suits the provider’s own operations. The conversation about engagement models accounting outsourcing UK for accounting outsourcing UK should start with the practice’s workload, not the provider’s preferred billing method.

The real cost of the wrong model

The wrong pricing model rarely announces itself through the headline rate. It shows up in the costs that don’t appear on the invoice. A practice that puts seasonal, variable work on a fixed retainer pays for capacity it isn’t using in the quiet months. One that runs predictable, high-volume work on a per-task basis often pays a premium per unit that a fixed arrangement would have undercut.

There are subtler costs too. Picking a model that doesn’t fit the workflow tends to generate rework, repeated onboarding as arrangements gets renegotiated, and the planning inefficiency of a cost base that won’t sit still. These don’t show on a quote, but they accumulate, and over a year they can dwarf the difference in headline rate that drove the original choice. The cheapest model on paper is frequently not the cheapest model in practice.

| Issue | Business Impact |

|---|---|

| Underutilised Retainer | Paying for unused capacity |

| Scope Creep | Reduced profitability |

| Variable Monthly Costs | Budgeting difficulty |

| Repeated Renegotiation | Administrative burden |

| Excessive Per-Task Charges | Margin erosion |

| Resource Bottlenecks | Missed deadlines |

What to look for in an outsourcing provider

The pricing model matters, but it sits on top of a more fundamental question: whether the provider is one worth building a relationship with at all. A keen price on either model is no bargain if the work is unreliable.

Transparency should drive the price

Whatever the model, the practice should understand how the figure is reached. A fixed price should come with a clear statement of what is in scope and what triggers an additional charge. A per-task price should come with a clear rate card and no ambiguity about what counts as a single unit of work.

Vagueness at the pricing stage is a reliable predictor of friction later. A provider that cannot or will not explain clearly how the cost is constructed is one to approach with caution.

Flexibility to expand the arrangement

A practice tends to grow and expand its operations overtime. The right outsourcing relationship should change with the times, moving work between fixed and per-task structures as volumes stabilise or as the practice grows. A provider that treats the initial pricing model as permanent, and resists revisiting it as the practice evolves, is offering a less useful relationship than one that expects the structure to be reviewed periodically.

The best outsourcing pricing models UK firms adopt are not chosen once and left untouched. They are reviewed as the practice changes, with the structure adjusted to keep matching the shape of the work.

How to budget an outsourcing project

One practical anchor helps frame the whole budget decision. Most UK practices budget outsourcing at somewhere between 8% and 15% of gross fee income, with the exact figure depending on service mix and growth ambition. A firm spending well below that range may be under-using outsourcing relative to its capacity needs. One spending well above it, without a clear growth strategy behind the expenditure, may have a model that isn’t matched to its workload.

The percentage should serve as a checkpoint, not a target. It gives a practice a way to test whether its outsourcing spend is proportionate before getting lost in the detail of which pricing model produces the lowest per-unit rate.

| Practice Size | Recommended Range |

| Sole Practitioner | 5%-10% |

| Small Firm (1-10 staff) | 8%-12% |

| Growing Firm (10-50 staff) | 10%-15% |

| Scaling Practice (50+ staff) | 12%-18% |

Final Thoughts on Outsourcing Models for UK Practices

The pricing model question is, underneath, a question about risk and predictability, and where each party wants to carry them. Fixed price moves the volume risk onto the provider in exchange for the practice accepting a defined scope. Per-task keeps the flexibility with the practice in exchange for accepting variable cost. Neither distributes risk wrongly. They simply distribute it differently, and the right distribution depends on the practice.

What distinguishes the firms that get this right is not that they chose the cleverer model. It is that they understood their own workload well enough to match the model to it, kept the scope discipline that fixed price demands or accepted the variability that per-task brings, and treated the pricing structure as something to review rather than set in stone.

The model that works best for UK practices is the one that fits the specific practice. That sounds like an evasion, but it is the actual answer. A firm that assesses its own volume stability, its client billing logic, its appetite for cost certainty, and the maturity of the provider relationship will arrive at the right structure for its situation. A firm that picks a model because it is the one the provider led with, or because it is what a peer firm happens to use, is far more likely to find itself renegotiating within the year.