As parents, we all want the best for our kids, and financial planning plays a crucial role. In this series, we’ll dive into the UK’s Junior Pension scheme, a powerful tool for building a solid financial foundation for your child.

Financial planning isn’t just about saving; it’s about strategic growth. The earlier you start, the better. The Junior Pension scheme may seem distant for a child, but it’s never too early to begin securing their retirement. We’ll explore how this scheme works, its advantages, and how to kickstart your child’s financial journey.

Understanding Junior Pensions

In this segment, we’ll unravel the fundamental concepts of Junior Pensions, exploring what they are, their purpose, how they function, and the perks of initiating one for your child’s financial future.

Definition and Purpose of Junior Pensions

Junior Pensions, also known as Junior Self-Invested Personal Pensions (Junior SIPPs), are specialized savings accounts tailored for children in the UK. Their primary purpose is to secure your child’s financial future by allowing you to invest in their behalf. These pensions are designed to accumulate wealth over time, ultimately providing a comfortable retirement or financial cushion when your child reaches adulthood.

The Mechanics of How They Work

Junior SIPPs operate on a straightforward principle. Parents, guardians, or relatives can contribute up to £3,600 annually into the pension account on behalf of the child. These contributions are invested in various assets, such as stocks, bonds, and funds, with the goal of generating long-term growth. Importantly, these investments have the potential to benefit from compound interest over time, significantly boosting the pension’s value.

Key Features of the Junior Pension Scheme

The Junior Pension scheme in the UK comes with several important features that make it an attractive option for securing your child’s financial future. Let’s explore these key aspects in detail:

1. Annual Contribution Limits:

- The Junior Pension scheme allows parents, guardians, or relatives to contribute up to £3,600 annually on behalf of the child. This contribution limit is a generous allowance, enabling you to make substantial investments in your child’s pension fund each year.

2. Access Rules – When Can the Child Access the Funds:

- It’s important to note that the funds in a Junior Pension are locked away until your child reaches the age of 55. This long-term commitment ensures that the money is primarily reserved for their retirement. However, once your child turns 18, they gain limited access to the pension, allowing them to manage the investments and make contributions themselves.

3. Transferability and Flexibility of the Pension Fund:

- The Junior Pension scheme offers flexibility when it comes to managing the pension fund. You can choose from a wide range of investment options, including stocks, bonds, and funds, allowing you to tailor the portfolio to your child’s needs and risk tolerance. Additionally, if you move to a different provider or decide to consolidate pensions, you can transfer the Junior Pension fund without losing the tax advantages it offers.

In summary, the Junior Pension scheme in the UK offers an attractive package for building a secure financial future for your child. With annual contribution limits, tax relief benefits, a long-term perspective on fund access, and flexibility in managing the pension fund, it’s a powerful tool that can help you take a proactive approach to your child’s financial well-being. Stay tuned for more insights on optimizing your Junior Pension in our upcoming posts.

Benefits of Investing in a Junior SIPPs

Investing in a Junior Pension offers a multitude of advantages, making it a smart choice for securing your child’s financial future. Here are the key benefits:

1. Compound Interest:

- The magic of compound interest is a significant advantage of Junior SIPPs. By starting early, you give your child’s pension fund more time to grow. As the interest earned on the contributions generates additional earnings, this compounding effect can result in substantial wealth accumulation over the long term.

2. The Power of Starting Early and Exponential Growth Potential:

- Beginning to invest in a Junior Pension when your child is young leverages the power of time. The earlier you start, the greater the potential for exponential growth. The contributions made during childhood can significantly multiply in value by the time your child reaches retirement age, providing a comfortable financial cushion.

3. Tax Benefits:

- Junior Pensions come with attractive tax benefits. When you contribute to the pension fund, the government provides a 20% tax relief, effectively boosting your contributions. This tax-efficient growth allows you to maximize your savings and achieve better returns on your investments.

4. Securing the Future:

- A Junior Pension is a forward-thinking investment that helps secure your child’s financial future. It ensures they have a nest egg to rely on when they reach retirement age, reducing the financial burden on them and giving you peace of mind knowing they’re financially secure.

5. Educational Tool:

- Investing in a Junior Pension also serves as a valuable educational tool. It teaches your child about the importance of financial planning and responsibility from an early age. Involving them in the process can instill good financial habits and a sense of ownership over their financial future.

In conclusion, a Junior Pension is more than just a financial investment; it’s a strategic move towards building a solid financial foundation for your child. With the benefits of compound interest, tax advantages, future security, and educational opportunities, it’s a proactive way to ensure your child’s financial well-being. Stay tuned for more insights on managing and maximizing your Junior Pension in our upcoming posts.

Other Child Investment Alternatives in the UK

Besides Junior SIPPs, there are other investment choices for securing your child’s financial future in the UK:

1. Junior Individual Savings Accounts (JISAs):

- Features: Tax-advantaged savings accounts for children with a £9,000 annual contribution limit. Come in cash or stocks and shares variants.

- Benefits: Tax-free growth, investment flexibility, and unrestricted access at 18.

- Comparison with Junior Pensions: JISAs offer flexibility and tax-free growth but lack the long-term focus of Junior Pensions.

2. Child Trust Funds (CTFs):

- Features: Former government initiative for children born between 2002 and 2011, now replaced by Junior ISAs.

- Benefits: Tax-free growth, government contributions, and investment choices.

- Comparison with Junior Pensions: CTFs were versatile savings accounts; Junior Pensions are tailored for retirement planning.

3. Premium Bonds:

- Features: Unique savings option with a chance to win tax-free prizes in monthly draws.

- Benefits: Prize potential, capital security, and anytime withdrawals.

- Comparison with Junior Pensions: Premium Bonds offer excitement but lack guaranteed returns and tax advantages.

4. Comparative Analysis with Junior Pensions:

- Long-Term Focus: Junior Pensions excel in long-term retirement planning.

- Tax Benefits: Junior Pensions and JISAs offer tax advantages; others do not.

- Access Rules: Junior Pensions promote discipline with strict access rules; others offer more flexibility.

- Investment Options: Junior Pensions and JISAs provide various investment choices; Premium Bonds have none, and CTFs are phased out.

In conclusion, select the investment vehicle based on your goals and risk tolerance. Junior Pensions are ideal for long-term retirement planning, JISAs offer flexibility, Premium Bonds provide excitement, and CTFs have been replaced by Junior ISAs. Consult a financial advisor for tailored guidance.

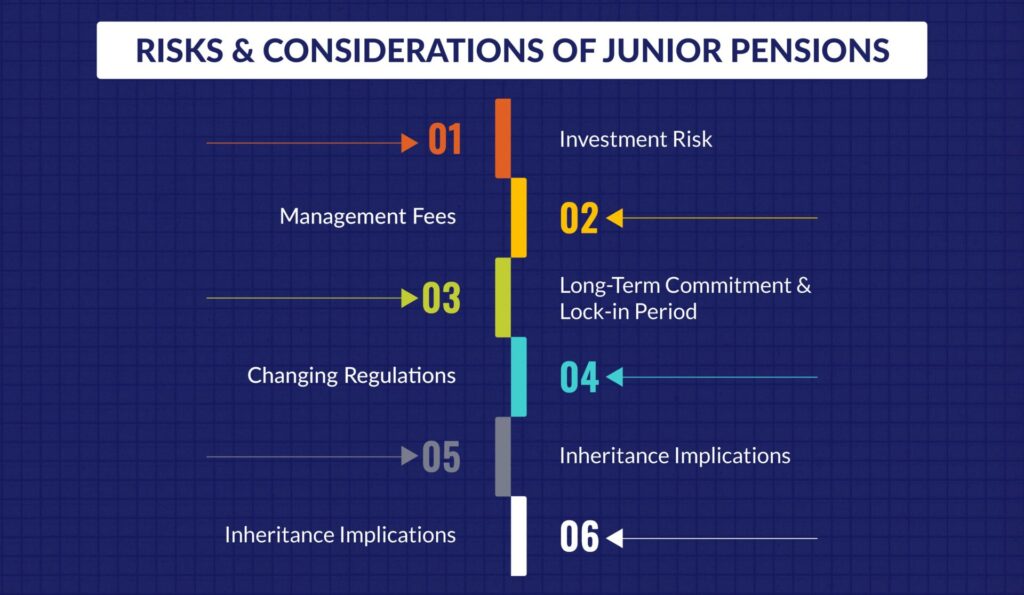

Potential Risks and Considerations of Junior Pensions

While investing in a Junior Pension or any other financial vehicle for your child’s future can be a wise decision, it’s crucial to be aware of potential risks and considerations. Here are key factors to keep in mind:

1. Market Volatility and Investment Risks:

- Market Fluctuations: Investments within Junior SIPPs can be subject to market volatility. The value of the investments can go up and down, which may impact the overall value of the pension fund.

- Risk Tolerance: Consider your child’s age and your risk tolerance when selecting investment options. As your child approaches the age when they can access the funds, you may want to shift towards lower-risk investments to protect the fund’s value.

2. The Importance of Reviewing and Potentially Changing Funds as the Child Ages:

- Changing Investment Strategy: Your child’s age and the time horizon until they can access the funds should influence your investment strategy. Younger children can afford to take on more risk, while older children may need a more conservative approach to preserve capital.

- Regular Review: Periodically review the performance of the investments within the Junior Pension and make adjustments as needed to align with your child’s evolving financial goals and risk tolerance.

3. Rules Around Accessing Funds and Potential Future Legislative Changes:

- Access Rules: Understand the access rules for Junior Pensions. Funds are typically locked until your child reaches age 55, but they gain some access at age 18. Be prepared for the potential need for funds when your child becomes an adult.

- Legislative Changes: Keep abreast of any legislative changes related to Junior Pensions or other child investment options. Government policies can impact contribution limits, tax benefits, and access rules.

4. Tax Considerations:

- Tax Implications: Be aware of tax implications when accessing funds. While contributions benefit from tax relief, withdrawals may be subject to taxation rules in place at the time of access.

5. Diversification:

- Risk Mitigation: Diversify investments within the Junior Pension to spread risk. A well-diversified portfolio can help mitigate the impact of poor-performing assets.

6. Financial Education:

- Teach Financial Responsibility: Use the Junior Pension as an opportunity to educate your child about financial responsibility. Involving them in discussions about savings, investments, and the importance of long-term planning can prepare them for future financial decisions.

To mitigate these risks and make informed decisions, consider seeking advice from a financial advisor who can provide personalized guidance based on your child’s specific circumstances and your investment goals. Regularly reviewing your investment strategy and staying informed about any changes in legislation will help ensure the Junior Pension remains a valuable tool for securing your child’s financial future.

Conclusion

In summary, early financial planning for your child’s secure future is paramount, and Junior SIPPs in the UK offer a potent solution. These pensions provide not only financial growth but also instill valuable life lessons. With tax advantages, flexibility, and growth potential, Junior Pensions are an intelligent choice for securing your child’s financial goals.

Key Takeaways:

- Early financial planning is crucial for your child’s secure future.

- Junior Pensions serve as both financial tools and educational resources.

- Tax benefits and flexibility make Junior Pensions a wise choice.

- Consult a financial advisor or pension specialist for personalized guidance.

- Consider outsourcing accounting services for expert insights into suitable pension plans.

Expert accountants can offer detailed insights into the most suitable pension plans, help you navigate complex financial matters, and ensure that your child’s financial future is in capable hands. Take the proactive step today to invest in your child’s tomorrow and watch their financial security flourish. Connect with us and learn more.

If you enjoyed reading this article, be sure to explore our other blogs on Accounting, Tax, and Outsourcing!