Quick Summary

Transitioning compliance-only clients to opt for the CAAS model requires CPA firms to analyze their most loyal clients to identify the ones that are the most suitable to receive the service. For such clients to make the transition, they need to follow a proper strengthening procedure while maintaining trust and credibility in their relationships.

Launching Client Accounting and Advisory Services (CAAS) is one of the most effective ways for CPA firms to increase recurring revenue and build stronger, long-term client relationships. The MAP survey from the AICPA shows that firms providing strategic financial advisory services saw a 19% growth in revenue.

However, building a CAAS practice is only half the challenge. The more difficult task is attracting clients, as this is the one aspect of the process that is not entirely within a firm’s control. CPA firms can invest in developing their advisory teams, refining their service offerings, and implementing the right technology. Ultimately, clients must recognize the value of advisory services and choose to make the transition from compliance-only engagements.

The good news is that many existing clients are already ideal candidates for advisory services; they simply may not realize they need them or understand the value they can receive. The key is shifting the conversation from completing historical compliance work to helping clients make better financial decisions for the future.

This blog discusses strategies CPA firms can use to identify ideal clients, communicate CAAS benefits, handle objections, and convert compliance engagements into advisory relationships.

Which Compliance Clients are the Best Candidates for CAAS?

Rather than trying to attract every existing compliance-related client, CPA firms must first develop the ability to identify which of their clients are best suited for advisory services. They should focus on clients who are most likely to see the value in such services, accompanying the CAAS pricing model. Pushing CAAS onto the wrong client can not only feel like an upsell but also potentially damage the client’s trust in the firm’s compliance-associated abilities. Instead, firms must have an internal filtering system. This system helps them identify which clients achieve the best results by analyzing specific signals in the financial data and behavior of existing clients. The following section lists the signs that depict whether a client is open to considering advisory services:

What Signs Indicate a Client is Ready for Advisory Services?

The most successful CAAS engagements begin with selecting the right clients not pitching advisory services to everyone. CPA firms should evaluate their existing compliance clients for specific financial, operational, and behavioral indicators that suggest they have outgrown traditional accounting services. Clients exhibiting one or more of the following signs are often facing challenges that compliance alone cannot solve, making them strong candidates for an ongoing advisory relationship.

| Readiness Signal | What It Looks Like in the Data | CAAS Service That Addresses It |

|---|---|---|

| Rapid business growth | Revenue jumps year-over-year, which outpace internal reporting capacity | Cash flow forecasting, hiring plans, and pricing strategy |

| Cash flow challenges | Healthy profit on paper, but tight or late payroll/vendor payments | Cash flow modeling, working capital analysis |

| Increasing operational complexity | New product lines, entity restructuring, margin volatility | Overhead allocation review, financial structure advisory |

| Expansion into new markets | Multi-state activity, new nexus exposure, multi-entity reporting | Scalable financial infrastructure, multi-entity reporting setup |

| Frequent questions outside tax season | Off-cycle calls/emails about hiring, pricing, major purchases | Ongoing advisory check-ins, fractional CFO support |

| Lack of budgeting or forecasting | No budget, no KPI tracking, reactive decision-making | Budget build, KPI dashboards, forecasting |

What is the Best Process for Transitioning Compliance Clients into CAAS?

The very process of choosing the correct clientele is an important step for a firm that wants to develop and broaden its offerings. After identifying the most appropriate clientele, a company will need to develop a clear and systematic process. This process should convert the chosen clients from compliance-based partnerships into advisory-based relationships. Such conversion should be done carefully to ensure that no harm will be done to the relationship and that it won’t be viewed as solely transactional in nature. The five-stage process described below is developed to help gain the necessary credibility and trust. Through such a process, a company can be assured that when it asks for the complete CAAS commitment, the client would already have felt the real value of the company’s offerings. It is much better than trying to persuade them just once during a sales presentation.

Step 1: Identify high-potential clients

Segment your current customer base with the criteria mentioned above. Companies generally employ a fairly simple system of rating their customers based on revenue growth, frequency of interaction, level of industry complexity, and profitability. This does not have to be complex either; a joint spreadsheet reviewed once a quarter by the partners and managers can help highlight the top 10-20 customers that should be targeted.

It’s also worth involving the staff who work closest with these clients. Tax preparers and bookkeepers often notice red flags, such as a client repeatedly asking the same financial questions, well before a partner does. Building a habit of flagging these clients internally creates a steady pipeline of CAAS opportunities.

| Client (example) | Revenue Growth | Off-Cycle Contact | Industry Complexity | Profitability | Advisory Tier |

|---|---|---|---|---|---|

| Client A | High | Frequent | Medium | Strong | High potential |

| Client B | Moderate | Occasional | Low | Strong | Medium potential |

| Client C | Flat | Rare | Low | Weak | Low potential |

| Client D | High | Frequent | High | Moderate | High potential |

Step 2: Assess advisory opportunities

With high-potential clients identified, the next step would be the conduct of further diagnostic analysis. In most cases, this analysis will involve looking into financial records over 12 to 24 months and highlighting issues that have not been addressed through compliance analysis. In other words, one needs to move from “This client seems promising” to “What does this client need?”

| Diagnostic Question | Why does it matter? |

|---|---|

| Is gross margin trending up or down? | Reveals pricing or cost-control issues the client may not see |

| How volatile is the monthly cash position? | Flags timing mismatches that cause payroll or vendor stress |

| Are the right KPIs being tracked for the industry? | Shows whether decisions are being made on relevant data |

| Is there any forward-looking financial visibility? | Indicates whether the client is planning or simply reacting |

Step 3: Present a value-based proposal

This is the step where many firms stumble. Presenting CAAS as a generic add-on service, priced by the hour, rarely resonates. Instead, the pitch should center on the needs uncovered in Step 2, focusing on goals the client truly cares about, such as enhanced visibility into cash flow, faster decision-making, or a clearer way forward toward the next level of growth.

Here are some tips that will help you sell your advisory services more effectively:

Speak from the client’s perspective. The best way to do this is to talk from the client’s data. Nothing is more powerful than being able to show a client their cash flow variability over the last year, or how they stack up against industry standards in terms of margins.

Speak in their language, not the language of accounting. Your clients likely don’t speak in terms of “fractional CFO services.” They think about making payroll or hiring employees. The following points list a few of the focus points that a CPA firm should maintain when presenting the value proposition of its CAAS model:

- Lead with outcomes, not services

- Support your recommendations with data

- Quantify the potential impact

- Provide a clear roadmap

- Address concerns proactively

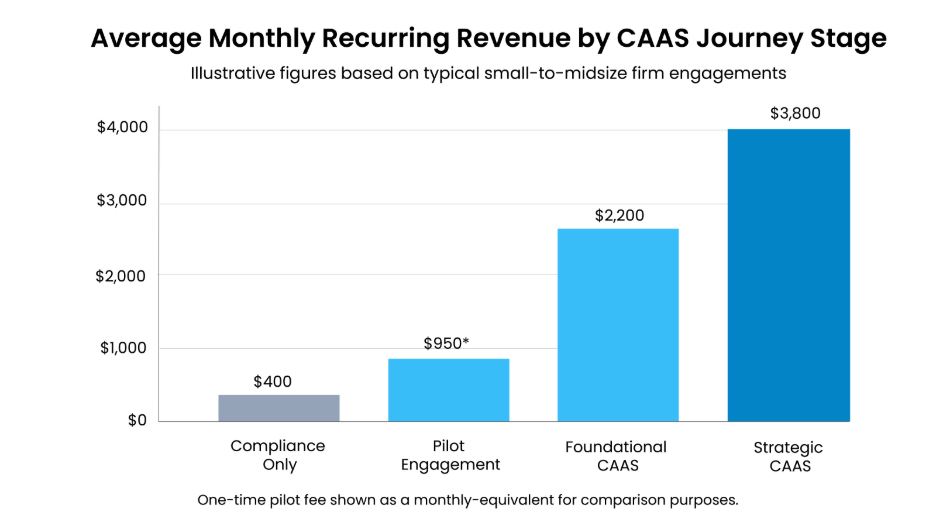

Step 4: Deliver a small advisory engagement first

Forcing a compliance-only client to make the commitment to a comprehensive and ongoing CAAS arrangement all at once is generally too much of a step to ask. The firm can offer a smaller, more concrete type of engagement, such as a one-off cash flow projection, budget construction, or financial system cleanup. This allows the client to sample advisory services with minimal risk. This stage is important for its ability to create evidence and build trust. An effective pilot will be able to prove the advisory capability of the firm without having the client take the firm’s word for it. The pilot will also give the firm the chance to show how ongoing advisory could have helped the client avoid an issue.

Step 5: Expand into an ongoing CAAS relationship

When the pilot engagement has been successfully completed, the natural evolution will be to move on to making the engagement a recurrent process. The firm will need to offer a way forward here. This can include monthly or quarterly reviews, ongoing forecasting, KPI reporting, or fractional CFO/controller support. There are also other options that may fit the needs of the customer and their budget.

This approach will be most effective when the firm highlights some of the results of the pilot. If a single forecast of cash flow helped a customer avoid a difficult month, then this would be a tangible outcome that can be offered as an argument for further monitoring.

It’s also worth setting expectations early that CAAS relationships evolve. If the client begins with the basic reports and forecasts, he or she can, after six or twelve months, be in a position to do strategic analysis such as budgeting for growth or raising capital. In looking at the CAAS services not as an endpoint but as a relationship, the scope can be expanded as confidence builds up.

Key Takeaways

Transitioning clients from compliance-only engagements to ongoing CAAS relationships isn’t about making a sale; it’s about helping clients solve increasingly complex financial challenges. It’s about acknowledging the pains that clients experience regarding their finances and showing how to overcome these pains. Successful transitioning firms typically employ several foundational strategies. They rely on financial data for decision-making rather than guesswork. When developing proposals, they address client-specific issues and utilize well-executed pilot projects to persuade, rather than relying on a single sales pitch.

However, what is most important here is that the client relationship in the context of transition is perceived as developing rather than static. A client who started out as a user of one forecast project might become an advisory client within a year if the firm is able to continue adding value in the course of this process. This is why the investment in the process described is rewarding for CPA firms.