As the owner of an accounting practice, one of your primary objectives is to maintain relevance within the industry. However, without a well-defined growth strategy for your accounting practice, it can be challenging to gain an objective perspective on what’s effective and what isn’t.

For Accounting Practice seeking to select the right software solutions for enhanced client management, workflow automation, and data-driven decision-making, these factors play a crucial role in fostering growth.

In this blog, we will delve into the strategies and tactics that can propel the growth of your Accounting Practice. We will explore various approaches to achieve exciting and measurable outcomes for your business.

Over the past decade, the accountancy landscape has experienced significant transformations that have reshaped the way professionals operate and serve their clients. An overview of significant changes:

- Digital Revolution: The arrival of cloud computing and sophisticated accounting software has revolutionized how financial data is managed. Automation and data analytics have become integral to modern best practices for accounting, streamlining processes, and reducing manual errors.

- Regulatory Complexity: Tax laws and regulations have grown increasingly complex, demanding accountants to stay vigilant and adapt swiftly to ensure compliance for their clients.

- Rise of Advisory Services: Accountants now do more than just crunch numbers; they also help with important strategies. They now offer services like financial planning, forecasting, and business consulting, adding significant value to their clients’ operations.

- Remote Work: The COVID-19 pandemic accelerated the adoption of remote work in the accounting industry. Virtual collaboration tools and secure remote access to financial data have become essential.

Accounting Practice’s Growth: Future Trends and Predictions

- Advanced Technology Integration: Artificial intelligence and machine learning will continue to play a pivotal role in automating repetitive tasks and providing data-driven insights. Blockchain technology may also find applications in enhancing transparency and security.

- Data Security and Privacy: As cyber threats evolve; accountants will need to invest further in robust cybersecurity measures and ensure strict adherence to data privacy regulations like GDPR and CCPA.

- Environmental, Social, and Governance (ESG) Reporting: ESG considerations will become mainstream as companies seek to demonstrate their commitment to sustainability. Accountants will be at the forefront of ESG reporting and auditing.

- Remote Work Continues: The remote work trend is likely to persist, with hybrid models becoming more prevalent. Accountants will need to maintain efficient virtual collaboration and client communication practices.

- Continued Education: Lifelong learning will remain crucial as the profession evolves. Accountants will need to stay updated on emerging technologies, regulatory changes, and industry best practices for accounting.

- Globalization: With businesses expanding internationally, cross-border taxation and compliance issues will become more complex. Accountants with expertise in international taxation will be in high demand.

In conclusion, the accountancy landscape has witnessed substantial changes in recent years, and it will continue to evolve rapidly. To thrive in this dynamic environment, accountants must embrace technology, stay vigilant on compliance fronts, expand their advisory roles, and prioritize ongoing education. As we look to the future, adaptability and innovation will be key to success in the ever-shifting sands of the accountancy profession.

Digital Transformation in Accounting Practices

As the Accounting Practices undergoes a profound digital transformation, it’s essential to understand and harness the power of emerging technologies. Here the key aspects of this transformation, including cloud accounting, artificial intelligence (AI) and machine learning, and integrated software solutions:

1. Cloud Accounting

One of the cornerstones of modern accountancy is cloud accounting. This revolutionary shift from traditional, on-premises systems to cloud-based platforms offer several advantages:

- Real-time Data Access: Cloud accounting provides instant access to financial data from anywhere, at any time. This real-time access enables accountants to make informed decisions and offer timely insights to clients.

- Flexibility: The flexibility of cloud-based solutions allows for scalability. As your client base grows or business needs change, you can easily adapt without the limitations of physical infrastructure.

- Security: Contrary to common misconceptions, cloud accounting often offers robust security features. Data is typically encrypted and stored on secure servers, reducing the risk of data loss due to hardware failure or physical theft.

2. Artificial Intelligence & Machine Learning

AI and machine learning are transforming the accountancy profession by automating tasks and enhancing analytical capabilities:

- Automating Repetitive Tasks: Mundane and repetitive tasks like data entry, invoice processing, and expense categorization can be automated. This not only reduces the risk of human error but also frees up valuable time for accountants to focus on strategic activities.

- Predictive Analysis: AI-driven analytics can provide predictive insights into financial trends and patterns. This helps accountants and businesses make proactive decisions based on data-driven forecasts.

3. Integrated Software Solutions

Integrated software solutions are another pivotal component of digital transformation:

- Streamlined Processes: Interconnected software tools enable seamless data flow between different functions, such as accounting, payroll, and inventory management. This streamlines workflows, minimizes data duplication, and enhances overall efficiency.

- Comprehensive Reporting: Integrated systems provide a holistic view of financial data, making it easier to generate comprehensive reports for clients and stakeholders. This simplifies financial analysis and decision-making.

In conclusion, embracing digital transformation in your accounting practices offers a multitude of benefits. Cloud accounting provides real-time data access, flexibility, and security. AI and machine learning automate tasks and offer predictive analysis capabilities, while integrated software solutions streamline processes and enhance reporting.

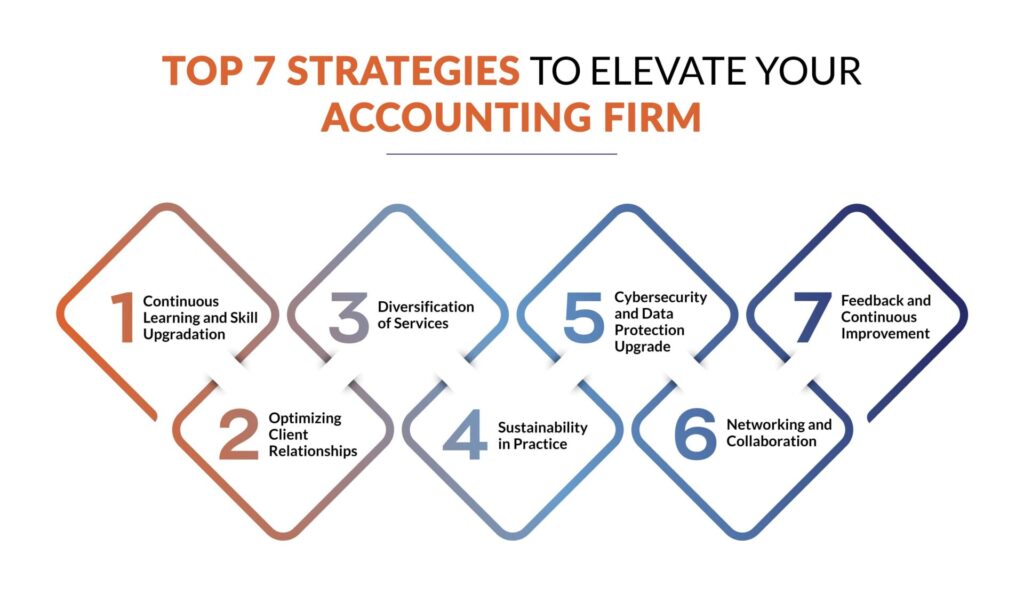

Top 7 Strategies to Elevate Your Accounting Practice

By leveraging these technologies, accountants can stay ahead in the evolving landscape, delivering more value to their clients and remaining competitive in an increasingly digital world.

1. Continuous Learning and Skill Upgradation

In the ever-evolving field of accounting practices, the importance of continuous learning and skill upgradation cannot be overstated. To thrive in the contemporary accounting scene, it’s crucial to stay abreast of the latest standards and regulations, promote continued education and certifications, and embrace emerging skills such as data analytics. Here are the detailed reasons for why it is so important:

1. Staying Updated with Accounting Standards and Regulations:

- Compliance and Accuracy: Accounting standards and regulations are subject to frequent updates and changes. Staying current ensures that accountants can maintain compliance and accuracy in financial reporting. Non-compliance can result in legal issues, financial penalties, and damage to a firm’s reputation.

- Quality Service: Clients rely on accountants to provide accurate and up-to-date financial information. Staying informed about the latest standards and regulations allows accountants to offer high-quality, reliable services that clients can trust.

- Adaptability: The ability to adapt to changing regulations demonstrates a commitment to excellence and a proactive approach to problem-solving. Accountants who stay updated are better equipped to navigate complex financial scenarios.

2. Encouraging Certifications and Additional Training:

- Professional Development: Encouraging certifications such as Certified Public Accountant (CPA), Chartered Accountant (CA), or Certified Management Accountant (CMA) showcases a commitment to professional development. These certifications demonstrate a high level of expertise and knowledge in the field.

- Competitive Advantage: Certified accountants often have a competitive edge in the job market. They tend to command higher salaries and can access a broader range of career opportunities.

- Specialization: Certifications also allow accountants to specialize in areas such as forensic accounting, tax planning, or internal auditing. This specialization can be a valuable asset to both accountants and their clients.

3. Rise of Non-Traditional Skills in Accounting Practices, like Data Analytics:

- Data-Driven Decision-Making: In today’s data-rich environment, accountants who possess data analytics skills can offer a new level of insight to clients. Analyzing financial data can uncover trends, efficiencies, and opportunities for improvement.

- Strategic Advisory: Accountants with data analytics skills are well-positioned to transition from traditional number crunching to strategic advisory roles. They can help clients make data-driven decisions that can drive business growth and profitability.

- Future-Proofing: As automation and AI become more prevalent in routine accounting tasks, non-traditional skills like data analytics become increasingly important for job security and career growth.

In conclusion, continuous learning and skill upgradation are paramount in the field of accountancy. Staying updated with accounting standards and regulations ensures compliance, accuracy, and adaptability.

2. Optimizing Client Relationships

Cultivating strong client relationships is essential for the success of any thriving accounting practice. To fortify these connections, it is crucial to employ strategic approaches, such as harnessing the potential of client portals, shifting focus toward advisory services, and maintaining regular and tailored communication.

Let’s delve into the specifics of each strategy:

1.Client Portals:

- Secure Platforms for Document Sharing and Collaboration: Client portals are secure online platforms that facilitate the exchange of financial documents and information. They offer a centralized and organized space for clients and accountants to collaborate.

- Efficiency and Transparency: Client portals enhance efficiency by reducing the need for back-and-forth emails and physical document transfers. They also provide transparency, allowing clients to access their financial data and updates in real-time.

- Data Security: Client portals prioritize data security, protecting sensitive financial information from unauthorized access. This security builds trust and reassures clients that their data is in safe hands.

2. Advisory Services

- Shifting from Pure Accountancy to Financial Consultancy and Advice: Accountants are no longer just number crunchers; they have evolved into trusted financial advisors. Offering advisory services, such as financial planning, tax optimization, and strategic financial advice, adds significant value to the client-accountant relationship.

- Client-Centric Approach: Understand your client’s unique financial goals, challenges, and aspirations. Tailor your advisory services to address their specific needs and provide personalized solutions.

3. Regular Communication

- Adapting to Client’s Preferred Communication Channels and Frequency: Recognize that each client has their preferred mode of communication and frequency of updates. Some may prefer email, while others prefer phone calls or video conferences. Adapt to these preferences to ensure a seamless and responsive client experience.

- Proactive Updates: Don’t wait for clients to reach out with questions or concerns. Proactively provide updates on important financial matters, regulatory changes, or any potential opportunities or risks that may impact their financial situation.

- Feedback and Listening: Encourage clients to provide feedback and actively listen to their concerns and suggestions. Incorporate their feedback into your service approach to continuously improve the client experience.

In conclusion, optimizing client relationships in your Accounting Practices is essential for long-term success. Client portals enhance efficiency and security, advisory services transition accountants into trusted financial advisors, and regular communication tailored to client preferences strengthens trust and engagement.

By adopting these strategies, accountants can build lasting, mutually beneficial relationships with their clients, ultimately contributing to the growth and success of their practice.

3. Diversification of Services

Diversifying your services is a key strategy for staying competitive in the evolving accountancy landscape. Here are two crucial aspects of diversification to consider:

- Exploring New Service Areas:

Consider expanding into areas such as business consultancy, financial planning, or IT advisory. These additional services can meet the growing demands of clients seeking comprehensive financial guidance.

- Adapting to Client Demands and Industry Trends:

Stay attuned to client needs and evolving industry trends. Regularly assess your service portfolio and be prepared to adjust it to align with current market demands. Flexibility and responsiveness are essential for sustained success of your Accounting Practice.

4. Sustainability in Practice

Sustainability is no longer a buzzword; it’s a necessity. Here’s how accountancy can embrace sustainable practices:

- Importance of Going Green:

Prioritize the adoption of environmentally friendly practices. This not only reduces your ecological footprint but also demonstrates your commitment to responsible business operations.

- Digital Solutions for Reduced Paper Waste:

Transition to digital solutions for document management, reducing the need for paper and minimizing waste. Digital document sharing and e-signatures are excellent alternatives.

- Energy-Efficient Office Solutions and Remote Work:

Implement energy-efficient office solutions, such as LED lighting and smart heating/cooling systems, to reduce energy consumption. Promote remote working options, which not only cut commuting-related emissions but also enhance work-life balance for your team.

By integrating these sustainable practices for accounting, Accounting Practices can contribute to a greener future while also improving operational efficiency and reducing costs.

5. Cybersecurity and Data Protection Upgrade

In today’s digital age, safeguarding sensitive data is paramount. Here’s how Accounting Practices can ensure cybersecurity and data protection:

- Recognizing Increasing Threats:

Acknowledge the growing cyber threats and the potential risks they pose to your accounting practice and clients. Understanding the landscape is the first step in addressing vulnerabilities.

- Investing in Top-Notch Security Solutions:

Allocate resources to invest in state-of-the-art cybersecurity solutions, including firewalls, intrusion detection systems, and robust encryption methods. Ensure that your systems are regularly updated to protect against emerging threats.

- Regular Training and Updates:

Conduct regular training sessions to educate your staff about potential threats, safe online practices, and the importance of maintaining data security protocols. Stay vigilant and adaptable in the face of evolving cyber risks.

By prioritizing cybersecurity and data protection, Accounting Practices can maintain the trust of their clients and safeguard sensitive financial information from potential breaches.

6. Networking and Collaboration

Networking and collaboration are integral to success in the accountancy field. Here’s why they matter:

- Affiliations with Industry Bodies:

Affiliating with industry bodies and organizations provides access to valuable resources, best practices for accounting, and industry insights. It also enhances your firm’s credibility and reputation.

- Collaborative Tools and Platforms:

Utilize collaborative tools and platforms to streamline communication and information sharing within your accounting practice and with clients. This enhances efficiency and strengthens relationships.

- Attending Conferences, Webinars, and Workshops:

Participation in industry events like conferences, webinars, and workshops fosters professional development, expands your knowledge base, and provides networking opportunities. Staying informed about emerging trends and technologies is essential for staying competitive.

By actively engaging in networking and collaboration, Accounting Practices can stay at the forefront of industry developments, foster meaningful connections, and offer enhanced services to their clients.

7. Feedback and Continuous Improvement

Achieving excellence in accountancy requires a commitment to feedback and continuous improvement:

- Importance of Client Feedback:

Client feedback is invaluable for optimizing services. Actively seek feedback to understand client needs, expectations, and areas for improvement. It strengthens client relationships and enhances service quality.

- Regular Internal Reviews and Audits:

Conduct regular internal reviews and audits to assess processes, identify inefficiencies, and ensure compliance with industry standards and regulations. This helps maintain high-quality service delivery.

- Adopting a Culture of Innovation and Flexibility:

Encourage a culture of innovation and flexibility within your firm. Embrace new technologies, methodologies, and best practices for accounting to adapt to evolving client demands and industry trends.

By embracing feedback and a commitment to continuous improvement, Accounting Practices can not only meet but exceed client expectations, ensuring long-term success and relevance in the field.

Conclusion

In the dynamic world of accountancy, agility and adaptability are the keys to success. By blending technology, continuous learning, and a client-centric approach, you can chart a course to stay ahead in this ever-evolving landscape.

Key Takeaways:

- Diversify Services: Expand into areas like business consultancy and adapt services to client needs.

- Embrace Sustainability: Go green, use digital solutions, and promote remote work for a smaller carbon footprint.

- Prioritize Cybersecurity: Invest in robust security, provide staff training, and stay vigilant against digital threats.

- Network and Collaborate: Affiliate with industry bodies, use collaborative tools, and attend events for growth.

- Feedback and Improvement: Collect client feedback, conduct regular audits, and foster innovation for excellence.

If you enjoyed reading this article, be sure to explore our other blogs on Accounting, Bookkeeping, and Outsourcing!

If you’re seeking ways to optimize and modernize your Accounting Practice, we’re here to help. Reach out for consultations and discover how embracing change and innovation can elevate your accounting practice to new heights. Contact us now to learn more.